The Shifting Sands of Global Prosperity

In the bustling corridors of power and the quiet hum of trading floors, a new economic reality is taking shape. As we navigate mid-2026, the global economy presents a paradox: pockets of remarkable resilience amidst a landscape increasingly defined by geopolitical tremors, persistent inflationary pressures, and the relentless march of technological disruption. This isn’t merely a period of adjustment; it’s a fundamental reordering, demanding a fresh perspective and a proactive strategy from leaders worldwide.

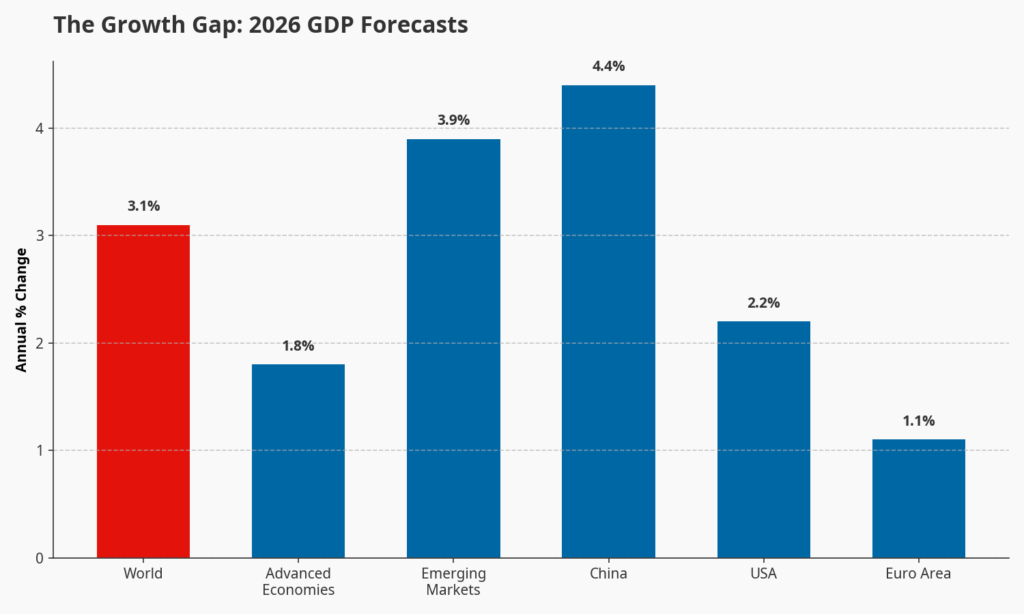

For years, the rhythm of global growth was predictable, albeit with its cyclical ebbs and flows. Today, that rhythm is punctuated by discord. The International Monetary Fund (IMF) and the World Bank, in their latest assessments, project a global Real GDP growth of approximately 3.1% for 2026 . While seemingly robust, this figure masks a stark divergence. Advanced economies, once the unwavering engines of prosperity, are decelerating. The Euro Area, for instance, is forecast to expand by a modest 1.1%, with the United States not far ahead at 2.2% .

Conversely, the dynamism is shifting eastward and southward. Emerging markets and developing economies (EMDEs) are poised to contribute significantly more to global expansion, with a projected growth rate of 3.9%. China, despite its own structural challenges, is expected to lead this charge with a formidable 4.4% growth . This disparity isn’t just about numbers; it’s about the uneven distribution of opportunity and the widening gap between those economies that have adapted and those still grappling with the aftershocks of a tumultuous half-decade.

The chart below illustrates the projected GDP growth across key global regions for 2026, highlighting these disparities.

The Storm Clouds on the Horizon

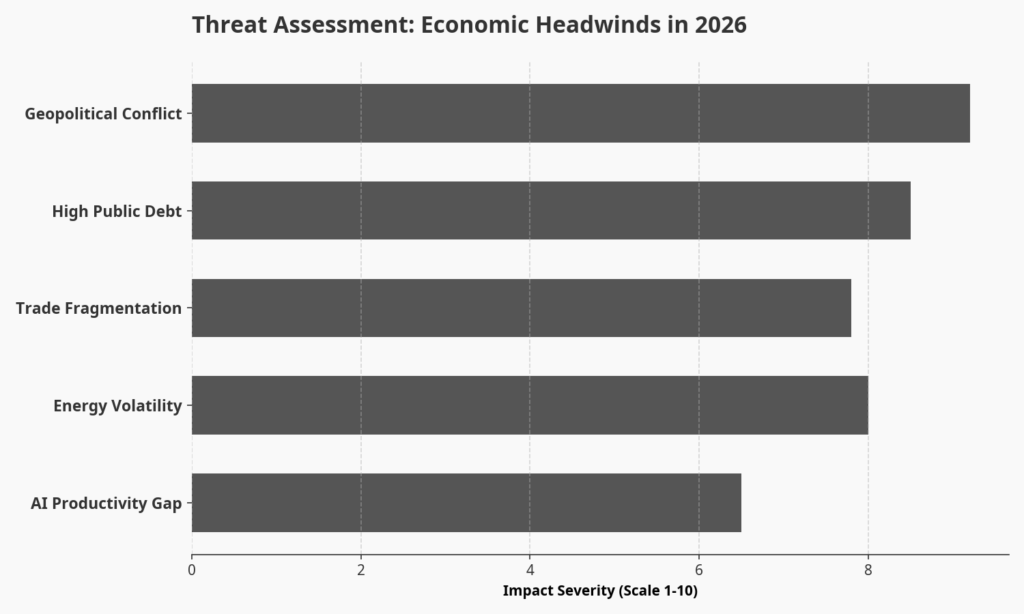

Beneath the surface of these growth figures lie potent risks that threaten to derail even the most optimistic projections. The most immediate and visceral concern remains geopolitical instability. The ongoing conflict in the Middle East, particularly involving Iran, casts a long shadow, not only disrupting supply chains but also fueling energy price volatility that reverberates through global markets . This isn’t just a regional issue; it’s a global inflationary accelerant.

Adding to this precarious balance is the specter of high public debt. Years of unprecedented fiscal stimulus, while necessary during crises, have left many nations with bloated balance sheets. This limits their ability to respond to future shocks and creates a delicate balancing act between fiscal prudence and the need for continued investment in public services .

Furthermore, the once-unquestioned tenets of globalization are being challenged by trade fragmentation. A rise in protectionist policies and the re-shoring of critical industries are reshaping global commerce, forcing businesses to rethink their supply chain resilience and geographical dependencies . The era of seamless, just-in-time global logistics is giving way to a more complex, just-in-case regionalized approach.

And then there’s the AI productivity gap. While artificial intelligence holds immense promise for boosting efficiency and innovation, its widespread adoption and the realization of its full economic benefits are still nascent. The gap between AI’s potential and its current impact represents both a challenge and an opportunity for nations and corporations alike . Finally, the energy shock, as underscored by the OECD, highlights the urgent need for a strategic and accelerated transition away from volatile fossil fuel markets towards more stable and sustainable energy sources .

The following chart visualizes the perceived impact severity of these key economic risks.

The Global Executive’s Playbook: 10 Decisions for 2026

In this environment of heightened uncertainty and rapid change, passivity is not an option. Leaders must adopt a proactive and adaptive mindset. Here is a ten-point playbook designed to guide strategic decision-making in 2026 and beyond:

1.Prioritize Geopolitical Risk Mitigation: Proactively assess and mitigate geopolitical exposures. This means diversifying supply chains away from known flashpoints, exploring near-shoring or friend-shoring strategies, and implementing robust hedging mechanisms against energy price and commodity volatility. Resilience, not just efficiency, must be the new mantra.

2.Accelerate AI Integration for Productivity Gains: Move beyond pilot programs and integrate AI at scale across operations. Invest aggressively in AI infrastructure, talent development, and ethical AI frameworks. The goal is to leverage AI not just for cost reduction, but for fundamental business model innovation and competitive advantage.

3.Implement “Fiscal Fortification” Strategies: Governments must embark on credible, long-term fiscal consolidation plans. This involves re-evaluating spending priorities, optimizing revenue collection, and exploring innovative financing mechanisms to reduce public debt without stifling growth or undermining social safety nets.

4.Adopt a “Fragmented Trade” Playbook: Businesses need to adapt to a world of regionalized trade blocs and increased protectionism. This entails building more localized supply chains, understanding complex tariff landscapes, and strategically engaging with regional economic partnerships to ensure market access and operational continuity.

5.Strategic Energy Transition Re-alignment: Accelerate investments in renewable energy and energy efficiency. This is not merely an environmental imperative but a strategic economic one, reducing vulnerability to global energy shocks and fostering long-term energy independence and cost stability.

6.Focus on “Resilient Emerging Markets”: Investors should meticulously identify and engage with EMDEs demonstrating strong domestic demand, sound macroeconomic policies, and relative insulation from geopolitical turbulence. These markets offer compelling growth narratives distinct from the slowing advanced economies.

7.Dynamic Inflation Management: Central banks must maintain a delicate balance, avoiding premature declarations of victory over inflation while remaining flexible enough to respond to evolving economic data. Clear communication and data-driven decision-making will be paramount to anchor expectations.

8.Invest in “Human Capital Adaptability”: The dual forces of AI and demographic shifts necessitate massive, ongoing investment in workforce reskilling and upskilling. Education systems and corporate training programs must evolve rapidly to equip the workforce with the skills needed for future economies.

9.Strengthen International Cooperation Frameworks: Despite rising nationalism, global challenges like climate change, pandemics, and debt crises demand renewed international collaboration. Leaders must seek common ground on trade standards, environmental policies, and financial stability to prevent a fragmented world from becoming a poorer one.

10.Defense-Growth Balancing Act: For nations increasing defense spending, careful consideration must be given to its macroeconomic impact. While it can stimulate short-term activity, it must be financed sustainably to avoid crowding out private investment, exacerbating debt, or diverting resources from critical social and economic development.

The global economy of 2026 is a testament to both human ingenuity and enduring fragility. The path forward is not one of passive observation but of decisive action. By understanding the underlying currents of change, mitigating the palpable risks, and embracing a strategic playbook that prioritizes adaptability, innovation, and sustainable growth, leaders can not only navigate the present turbulence but also lay the groundwork for a more prosperous and equitable future. The challenge is immense, but so too is the opportunity for those willing to lead with foresight and courage.

References

[2] World Bank. (n.d.). Global Economic Prospects.

[3] S&P Global. (2026, May). Global Economic Outlook: May 2026.