The Death of Peace Dividend

In the 1990s, after the fall of the Soviet Union, the security environment fundamentally changed. With the immediate threat of a major superpower conflict vanishing, nations took the opportunity to capture what economists call “Peace Dividend”; shifting massive military expenditure into productive and welfare investments. This resulted in tax cuts and returning the wealth to the public sector. Expenses on public infrastructure, civilian technology, education, social services and the national healthcare system increased aggressively.

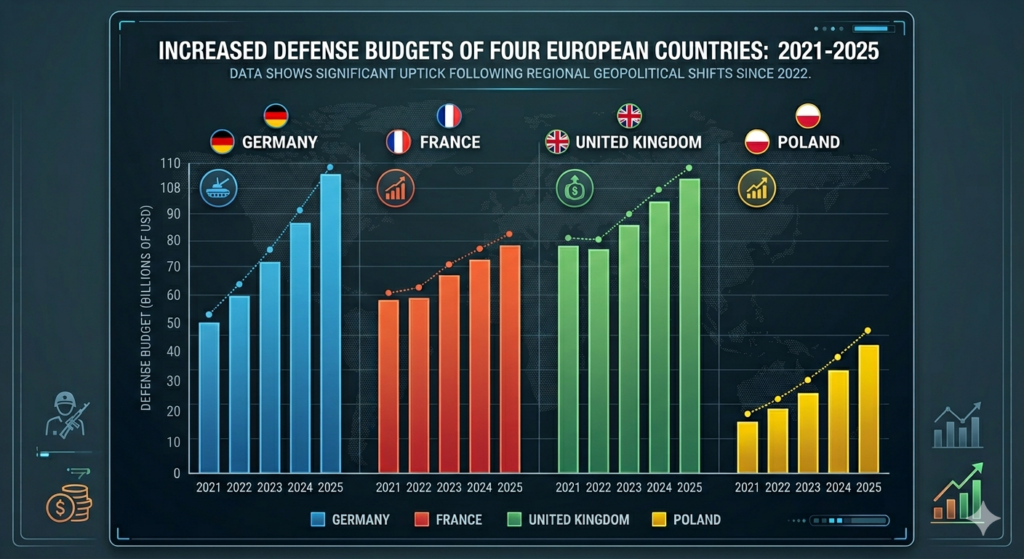

From this to dramatic shift of European countries doubling their military budgets and in some cases tripling them is driven primarily by the Russian invasion of Ukraine. This war marked the end of the 1990s “Peace Dividend” era. European countries are now running from military underinvestment to a state of urgent conventional deterrence. After 2015, European nations and Canada have more than doubled their collective defense spending, marking an increase of 106%($574 billion). On an individual level, only Germany has increased their defense budget from $56 billion to $108 billion between 2021 and 2025. The re-election of Trump in the USA has also forced European countries into stark reality as they no longer could rely on the US security umbrella. That’s why Europe is investing in autonomous defense systems for a reduction in American support.

All these events act as a “crowding out” effect. Unlike the USA, European countries’ economic models are built on a welfare state. The European Commission on Macroeconomic Analysis notes that higher defense budgets are actively eating up the fiscal budget for health,education, and public infrastructure. Billions of euros originally intended for green energy transition initiatives are getting recalled to fill up security investments. Defense driven expenditures also increase the debts of those nations. Corporate expansion is also getting hampered due to lack of investment in this sector, structurally weakening the real investment returns.

Supply chain Duplication as an inflationary floor

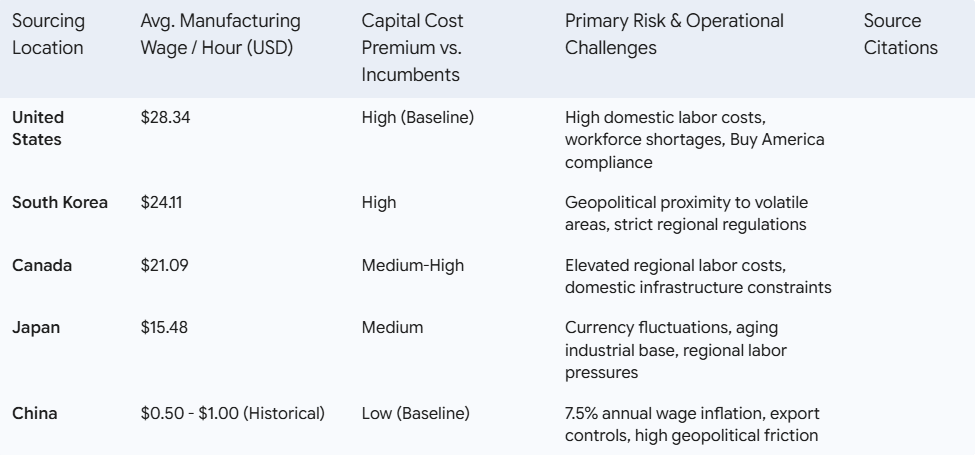

Building factories in friendly nations is obviously safer when global politics is messy. But it is more expensive compared to sticking with a low cost global provider. For a long time, companies runned after thin margins by putting their eggs in one basket. Moving those industries to friendly nations means paying massively. Higher wages, strict environmental laws, and duplicate facilities. It ultimately pulls back those businesses from the global bottom line.

A series of global events such as COVID-19 pandemic, Russia – Ukraine war, ongoing crisis in the middle east has exposed the deep vulnerabilities of global business and its sourcing. After witnessing this volatile landscape; policy makers and corporate leaders are giving priority to resilience over optimization. This state created three restructuring mechanisms.

- On-shoring: critical production directly back to the domestic market.

- Near-shoring: shifting manufacturing hubs to geographically adjacent regions to minimize lead time, reduce logistic costs and improve market responsiveness.

- Friend shoring: Gathering manufacturing and sourcing networks within nations regarded as stable economic,political and military allies.

The rare earth materials market is valued more than $320 billion. China controls approximately 60% of rare earth material processing. China also controls 70% of global lithium chemical conversion,while Indonesia holds over 60% of the global nickel supply. This highly concentrated footprint exposes the manufacturers monopoly.

To mitigate this risk, western countries are now investing billions to establish their own supply chain. The US,Europe and Australia are working to cut mineral import dependency by 50% by 2029.

Energy transition vs Energy security

The war in the middle east has acted as a fuel for this debate. Governments are shifting back to strategic petroleum reserves to maintain basic stability. To prevent blackouts and economic collapse,many nations have temporarily suspended incentivized domestic fuel production to bridge the gap left by disrupted imports. The blockade of the strait of Hormuz in March 2026 proved that relying on imported gas and oil from volatile regions is a fundamental national security risk.

This crisis accelerated the adoption of EVs and solar pumps not just for the environment,but to disintegrate household costs from global oil price volatility.

The divergence of “Global South”

While the west and china are decoupling, connector economies like India, Indonesia, Brazil, Poland are the primary beneficiaries. They practice active non alignment, refusing to pick sides between the USA and Russia/China. These countries benefit from “Multi alignment”. When the US moved their critical component factories out of China, they landed in India or Vietnam. Simultaneously, these nations import cheap energy from Russia and infrastructure investment from China. They are gaining geopolitical rent, extracting profit from both sides in exchange for staying neutral.

These countries act as connectors,but that role is only viable as long as the US and China allow it. In 2026, the US is giving continuous objection to Chinese goods assembled in Mexico or Vietnam. If the US decides that these countries are merely a “back door” for Chinese components to bypass tariffs, they could face retaliatory tariffs. As global powers move towards “industrial policy” connector economies are forced to pick sides. A neutral stance is getting harder to maintain.

Unlike the US, many global south hubs like India and Vietnam rely on imported oil and gas. In 2026, disruptions in the Middle East exposed their dependency on external fossil fuel and caused cascading costs that resulted in domestic inflation, forcing their central banks to keep rates high even when growth slowed down. Moving a factory to these countries adds resilience but often adds 15-20% in logistic loss in the form of higher prices which is passed to local workers and consumers. While these nations are setting up factories, they may not be able to train their workforce fast enough for high tech manufacturing.